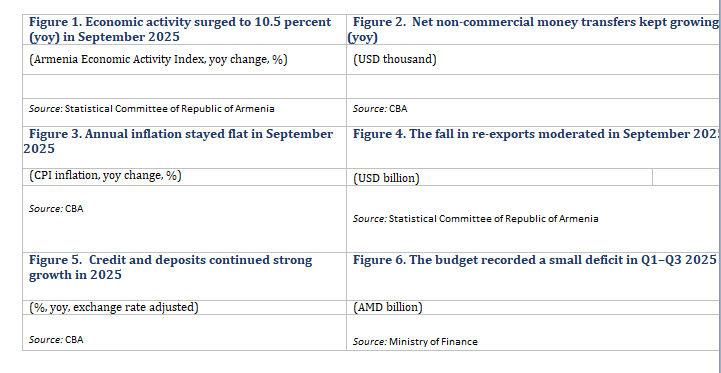

- Growth surged to 10.5 percent (yoy) in September, driven by food and metal production.

- Net non-commercial money transfers rose 16.2 percent (yoy), driven by inflows from Russia.

- Inflation stayed flat at 3.7 percent in October, and the CBA kept the refinancing rate unchanged.

- The phasing out of the re-export of precious stones and metals continued in September.

- At 0.73 percent of annual projected GDP, the Q1–Q3 deficit remained below forecasts.

In September, growth in economic activity was robust at 10.5 percent (yoy), up from 7.5 percent (yoy) in August (Figure 1). This was due to industrial growth almost doubling, with output growing 10.1 percent (yoy) in September, up from 5.8 percent (yoy) in August. Manufacturing grew 12.1 percent (yoy), driven by greater food production and continued expansion in base metal production. Mining activity grew 1.8 percent (yoy), following flat growth in August. Construction remained strong, growing at 22 percent (yoy). Services (excluding trade) expanded 7.9 percent (yoy), compared with 6.7 percent (yoy) in August. Trade (wholesale and retail) eased to 0.9 percent (yoy). Cumulative yoy growth for Q1–Q3 2025 stood at 7.6 percent, far exceeding initial expectations. After a 3.5 percent fall in August, monthly business registrations shot up 26.8 percent (mom), due to a 32 percent (mom) increase in registrations by individual entrepreneurs and a 14.2 percent (mom) increase in LLC registrations.

In September, net non-commercial money transfers continued double-digit growth (16.2 percent, yoy). This was driven by a 60 percent (yoy) increase in net inflows from Russia, representing 63 percent of total net inflows, and a 3.7 percent (yoy) rise in net inflows from the United States (Figure 2).

In October, inflation stabilized at 3.7 percent (yoy) (Figure 3). Inflation in food and non-alcoholic beverages (at 5.6 percent, yoy) remained the main contributor to October’s inflation (61 percent of the total increase). On November 4, Armenia’s Central Bank (CBA) decided to maintain the policy rate at 6.75 percent, marking the sixth consecutive meeting without a change to the rate.

In September, contraction in exports and imports moderated, due to the phasing out of re-exports (Figure 4). Exports fell 24.4 percent (yoy) in September compared with 40.8 percent (yoy) in August. Imports fell 19.5 percent (yoy), following a 28.3 percent (yoy) contraction in August. This was mostly driven by the fall in exports (down 67.2 percent, yoy) and imports (down 78.7 percent, yoy) of precious and semi-precious stones and metals. The fall in exports was also driven by contraction in livestock (down 30.4 percent, yoy); textiles (down 17.6 percent, yoy); and transport (down 15.2 percent, yoy). This was partly offset by increases in the export of minerals (up 56.3 percent, yoy); ready food products (up 20.5 percent, yoy); and machinery (up 14.5 percent, yoy). In September, excluding the re-export trade in precious metals and stones, exports and imports grew 16.7 percent (yoy) and 7.3 percent (yoy), respectively. Cumulative year-t-date-(ytd) exports contracted 46.8 percent (yoy), and imports fell 33.4 percent (yoy). In October, following a slow start in early 2025, Armenia’s tourist arrivals increased 4.4 percent (yoy), at a slower pace than over the summer.

Read also

In October, the AMD/USD exchange rate remained stable on average compared to the previous month. Compared to the same month last year, the AMD appreciated 1.2 percent (yoy) against the USD in October, while depreciating against the EUR and RUB 5.5 percent (yoy) and 17.7 percent (yoy), respectively. In September, the Real Effective Exchange Rate (REER) fell 1 percent (yoy). Gross reserves stabilized at USD 4.3 billion, equivalent to 3.4 months of import cover.

In September, commercial bank deposits grew 1.1 percent (mom) and credit expanded 2.1 percent (mom). Both increases continue to be driven by expansion in AMD-denominated funds. Credit growth was mostly driven by consumer and mortgage AMD loans, with a 45 percent share of total loans. Since January, mortgage loans, although sizeable, have been on the decline due to the phasing out of the income tax refund program. Exchange rate-adjusted annual growth stabilized at 16 percent (yoy) for total deposits and at 27.2 percent (yoy) for credit (Figure 5).

In September, a deficit equal to 0.1 percent of projected annual GDP was recorded. Tax revenues (including mortgage-related income tax) grew 8.7 percent (yoy) in nominal terms in September, driven by higher collection of VAT (up 25.4 percent, yoy); income taxes (up 10.7 percent, yoy); and profit taxes (up 12.6 percent, yoy). Social payments rose 13.3 percent (yoy) and turnover tax collection expanded 53.1 percent (yoy), due to the higher rate of turnover taxes in 2025. However, environmental tax collection fell 22.5 percent (yoy). Total expenditure increased 23 percent (yoy). Capital expenditure grew 79.5 percent (yoy), mostly driven by a 50.7 percent (yoy) rise in defense expenditure. Expenditure on education almost doubled (yoy) due to continuing school construction and rehabilitation plans. Current expenditure increased 7.8 percent (yoy) in nominal terms, driven mainly by social protection spending (up 8.9 percent, yoy). The cumulative Q1–Q3 deficit reached 0.73 percent of annual projected GDP, compared with the 5.5 percent of GDP deficit planned for 2025.

World Bank

2025: Results for Armenia and Other")