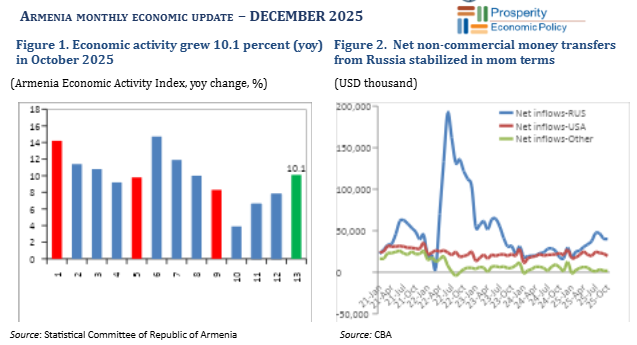

- Growth rose to 10.1 percent (yoy) in October, buoyed by construction and manufacturing.

- Net non-commercial money transfers rose 31.2 percent (yoy), driven by inflows from Russia.

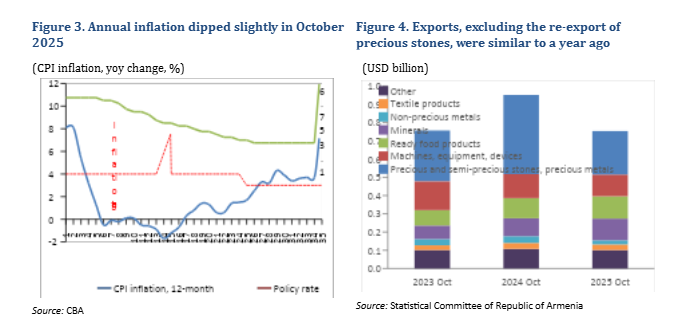

- Inflation dropped slightly in November, to 3.1 percent.

- Phasing out the re-export of precious stones and metals continued in October.

- A deficit equivalent to 1.4 percent of projected annual GDP was recorded in October.

In October, growth in economic activity remained in double digits, at 10.1 percent (yoy) (Figure 1), compared with 11.1 percent (yoy) in September. This was due to industrial growth rising to 17.9 percent (yoy) in October, as growth in mining and manufacturing accelerated to 15.9 percent (yoy) and 20.8 percent (yoy), respectively (up from September’s 1.8 percent and 12.1 percent, respectively). The surge in manufacturing was primarily due to a 2.3-fold increase in base metal production. Construction continued strong growth, at 20.1 percent (yoy). Services (excluding trade) expanded 12.8 percent (yoy), up from 9.9 percent (yoy) in September. Wholesale and retail activity stabilized at 1 percent (yoy), after robust growth in 2024. Cumulative yoy growth for January-October 2025 picked up to 8.1 percent (yoy), continuing to exceed initial expectations. The number of registered businesses, particularly individual entrepreneurs, was high in October for the second month in a row, exceeding 25 percent the January-August 2025 average.

In October, net non-commercial money transfers grew 31.2 percent (yoy), up from 16.2 percent (yoy) in September. This was driven by a 2.2-fold increase in net inflows from Russia (representing 65.3 percent of the total) in October, with net inflows from the United States contracting 14 percent (yoy), and 71.4 percent (yoy) from other countries. In mom terms, there has been a continued dip in inflows: 11 percent in September and 5 percent in October (Figure 2).

In November, annual inflation eased to 3.1 percent (yoy), down from 3.7 percent (yoy) in October (Figure 3). This was largely driven by lower inflation in food and non-alcoholic beverages of 3.8 percent (yoy) in November, down from 5.6 percent (yoy) in September.

In October, imports and exports continued to fall, due to the phasing-out of re-exports (Figure 4). Exports fell 21.8 percent (yoy) in October, following a 24.4 percent (yoy) decrease in September. Imports fell 11.9 percent (yoy), compared with 19.5 percent (yoy) in September. This was mostly driven by the fall in exports (down 45 percent, yoy) and imports (down 33 percent, yoy) of precious and semi-precious stones and metals. A contraction in exports of non-precious metals (down 39 percent, yoy) and machinery (down 9.4 percent, yoy) was also recorded. This was partly offset by increases in the export of minerals (up 21 percent, yoy); and ready food products (up 10.5 percent, yoy). In October, excluding the re-export trade in precious metals and stones, exports fell 0.5 percent (yoy), whereas imports grew 0.5 percent (yoy). Cumulative ytd exports and imports fell 44.7 percent (yoy) and 31.2 percent (yoy), respectively. In November, tourist arrivals grew 15.4 percent (yoy), compared with 4.4 percent (yoy) in October.

Read also

in November to 4.7 percent (yoy) in December, bringing annual growth to 8 percent")

In November, the AMD/USD exchange rate appreciated slightly on average, compared with October. Compared with November 2024, the AMD appreciated 1.8 percent (yoy) against the USD in November 2025 but depreciated 6.8 percent (yoy) against the EUR and 23.6 percent (yoy) against the RUB. Gross reserves grew to USD 4.6 billion, equivalent to 3.7 months of import cover.

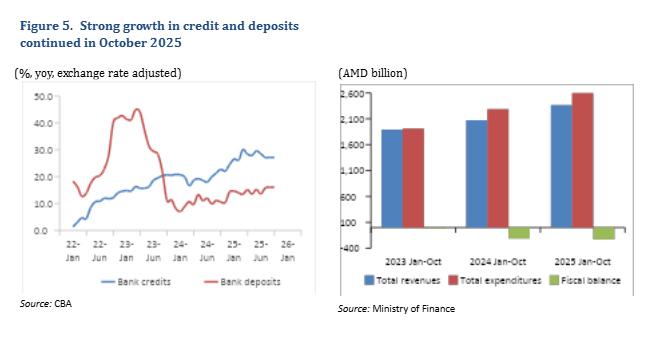

In October, commercial bank deposits grew 1.3 percent (mom) while credit expansion stabilized at 2.1 percent (mom). Credit growth remains concentrated in AMD consumer and mortgage loans, which, on average, make up almost 45 percent of the loan portfolio. While the (yoy) growth of consumer loans has been accelerating, the growth of mortgage loans has been slowly declining, reflecting the gradual phasing out of the mortgage interest refund program. Exchange-rate-adjusted annual growth remained stable in October, at 16 percent (yoy) for total deposits and at 27.2 percent (yoy) for credit (Figure 5).

The 1.4 percent of annual projected GDP deficit recorded in October was twice the total deficit over Q1–Q3. In October, tax revenues (including mortgage-related income tax) grew 13.7 percent (yoy) in nominal terms, driven by higher collection of income taxes (up 13.2 percent, yoy); profit taxes (up 46.5 percent, yoy); and VAT (up 4 percent, yoy). Social payments rose 10.3 percent (yoy). Turnover tax collection continued robust growth, at 29 percent (yoy), due to increased rates. The only decline was in the collection of customs duties (down 15.1 percent, yoy) and environmental taxes (down 0.7 percent, yoy). Total expenditure increased 11.5 percent (yoy). Capital expenditure grew 16.3 percent (yoy), largely driven by growth of 25 percent (yoy) in general public services and 10.7 percent (yoy) in defense expenditure. Expenditure on education grew 15.9 percent (yoy), as school construction and rehabilitation plans continued. Current expenditure increased 12.4 percent (yoy) in nominal terms, although social protection expenditure decreased 2.7 percent (yoy). The cumulative January-October deficit widened to 2.1 percent of annual projected GDP, with two thirds materializing in the month of October. This is still less than the projected annual deficit of around 5 percent of GDP.

External Affairs Officer

Europe & Central Asia (ECA)

World Bank Armenia

in January")

2025: Results for Armenia and Other")